Home

/ What Is A Non Qualified Plan : Executives often utilize nqdc plans to defer income taxeson their earnings.

What Is A Non Qualified Plan : Executives often utilize nqdc plans to defer income taxeson their earnings.

What Is A Non Qualified Plan : Executives often utilize nqdc plans to defer income taxeson their earnings.. Coverage under any other medical plan (primary or secondary/dependent coverage) will make you ineligible for an hsa plan. Qualified and nonqualified deferred compensation plans are both employee benefits for small business. This means any earnings on the investment are not taxed until they are paid out to the annuity holder. They differ drastically from qualified plans, like 401(k)s. Benefits received on or after january 1, 1997 will not be taxed, even if they:

You can invest as much or as little as you want in any given year, and you can withdraw at any time. There is a different set of rules for a qualified plan vs. This type of policy becomes paid up once a certain amount of premium has been paid into it. They differ drastically from qualified plans, like 401(k)s. Your employer gets to write off the cost of any fringe benefits, and.

What Are The Retirement Plan Dollar Limits For 2020 Lexology from d2dzik4ii1e1u6.cloudfront.net Differences between qualified & nonqualified plans. Failing to understand the rules can lead to problems for you and your employees. One of the main differences between the two is contribution limits. Executives often utilize nqdc plans to defer income taxeson their earnings. An annuity can be classified as non qualified money, but can grow tax deferred just like qualified money. A nonqualified (nq) plan is simply a plan that does not qualify under internal revenue code (code) section 401 (a), which includes standards for who can participate in the plan, how benefits are accrued, vesting schedules, distribution options, etc. Qualified and nonqualified deferred compensation plans are both employee benefits for small business. Nqdc plans (sometimes known as deferred compensation programs, or dcps, or elective deferral programs, or edps) allow executives to defer a much larger portion of their compensation and to defer taxes on the money until the deferral is paid.

Executives often utilize nqdc plans to defer income taxeson their earnings.

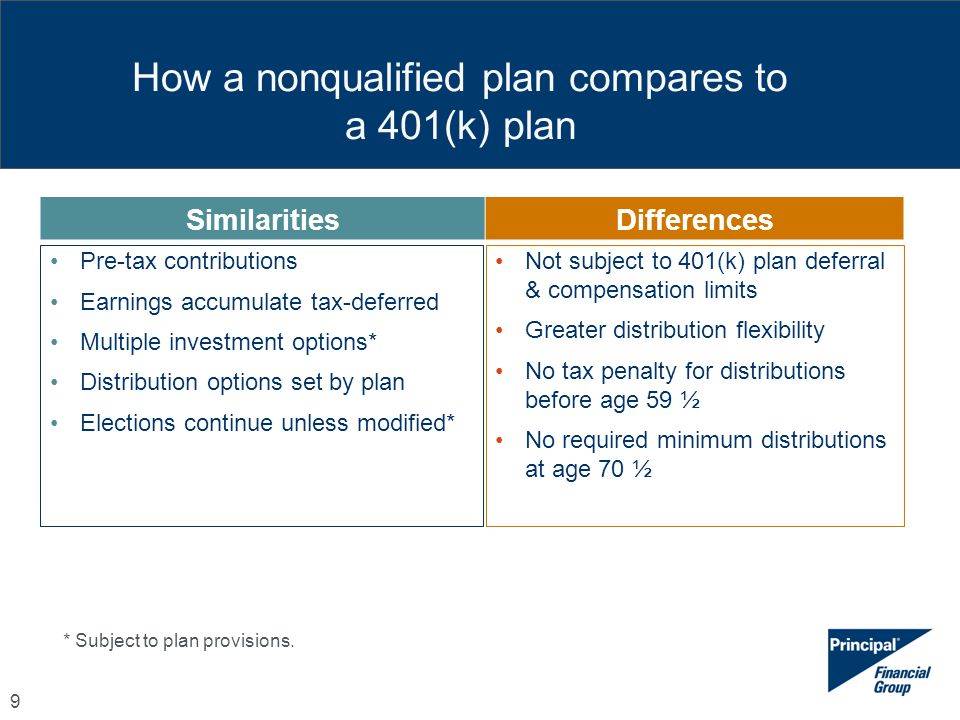

Executives often utilize nqdc plans to defer income taxeson their earnings. One popular type of non qualified retirement plan is an annuity. A nonqualified (nq) plan is simply a plan that does not qualify under internal revenue code (code) section 401 (a), which includes standards for who can participate in the plan, how benefits are accrued, vesting schedules, distribution options, etc. Your employer gets to write off the cost of any fringe benefits, and. Could i benefit from deferring income taxes until a later date? But, both are handled very differently. Nqdc plans (sometimes known as deferred compensation programs, or dcps, or elective deferral programs, or edps) allow executives to defer a much larger portion of their compensation and to defer taxes on the money until the deferral is paid. There are no caps or limitations on benefits. Qualified and nonqualified deferred compensation plans are both employee benefits for small business. Coverage under any other medical plan (primary or secondary/dependent coverage) will make you ineligible for an hsa plan. No portion of your premium is deductible. Always check with your insurance provider to see if your plan is hsa compatible. Differences between qualified & nonqualified plans.

Failing to understand the rules can lead to problems for you and your employees. A nonqualified plan can provide deferred payments at a specified future date, allowing you to save for certain life events, such as a child's college education. A nonqualified (nq) plan is simply a plan that does not qualify under internal revenue code (code) section 401 (a), which includes standards for who can participate in the plan, how benefits are accrued, vesting schedules, distribution options, etc. Qualified and nonqualified deferred compensation plans are both employee benefits for small business. You can invest as much or as little as you want in any given year, and you can withdraw at any time.

Nonqualified Deferred Compensation Plan Ppt Video Online Download from slideplayer.com The good news is that these plans often still allow employees to defer taxes until retirement but they aren't deductible to the employer and the employee has to pay taxes on the contributions right away. Nqdc plans (sometimes known as deferred compensation programs, or dcps, or elective deferral programs, or edps) allow executives to defer a much larger portion of their compensation and to defer taxes on the money until the deferral is paid. Also known as permanent insurance, cash value policies accumulate cash inside the policy from a portion of the premiums paid. A nonqualified deferred compensation (nqdc) plan is an arrangement that an employer and employee agree to where the employer accepts to pay the employee sometime in the future. In other words, all of your earnings on an non qualified annuity will not trigger an annual 1099 tax form from the annuity company. One popular type of non qualified retirement plan is an annuity. There are no caps or limitations on benefits. This means any earnings on the investment are not taxed until they are paid out to the annuity holder.

No portion of your premium is deductible.

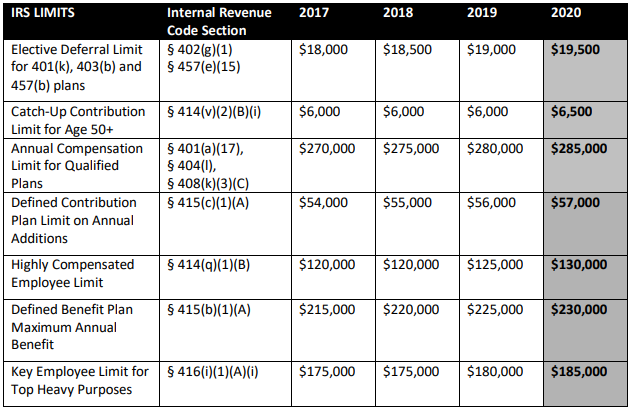

Executives often utilize nqdc plans to defer income taxeson their earnings. There is a different set of rules for a qualified plan vs. Contributions to qualified 401 (k) and 403 (b) plans are capped at $19,500 in 2021, the same as 2020. Qualified and nonqualified deferred compensation plans are both employee benefits for small business. A nonqualified plan can provide deferred payments at a specified future date, allowing you to save for certain life events, such as a child's college education. One popular type of non qualified retirement plan is an annuity. One of the main differences between the two is contribution limits. Nqdc plans (sometimes known as deferred compensation programs, or dcps, or elective deferral programs, or edps) allow executives to defer a much larger portion of their compensation and to defer taxes on the money until the deferral is paid. This type of policy becomes paid up once a certain amount of premium has been paid into it. An annuity can be classified as non qualified money, but can grow tax deferred just like qualified money. The good news is that these plans often still allow employees to defer taxes until retirement but they aren't deductible to the employer and the employee has to pay taxes on the contributions right away. This means any earnings on the investment are not taxed until they are paid out to the annuity holder. Coverage under any other medical plan (primary or secondary/dependent coverage) will make you ineligible for an hsa plan.

This type of policy becomes paid up once a certain amount of premium has been paid into it. Also known as permanent insurance, cash value policies accumulate cash inside the policy from a portion of the premiums paid. An annuity can be classified as non qualified money, but can grow tax deferred just like qualified money. Contributions to qualified 401 (k) and 403 (b) plans are capped at $19,500 in 2021, the same as 2020. Failing to understand the rules can lead to problems for you and your employees.

The Ultimate Guide To Qualified Versus Non Qualified Retirement Plans from www.moneyhacker.org An annuity can be classified as non qualified money, but can grow tax deferred just like qualified money. A nonqualified plan can provide deferred payments at a specified future date, allowing you to save for certain life events, such as a child's college education. Qualified and nonqualified deferred compensation plans are both employee benefits for small business. One of the main differences between the two is contribution limits. The good news is that these plans often still allow employees to defer taxes until retirement but they aren't deductible to the employer and the employee has to pay taxes on the contributions right away. One popular type of non qualified retirement plan is an annuity. Nqdc plans (sometimes known as deferred compensation programs, or dcps, or elective deferral programs, or edps) allow executives to defer a much larger portion of their compensation and to defer taxes on the money until the deferral is paid. In other words, all of your earnings on an non qualified annuity will not trigger an annual 1099 tax form from the annuity company.

Differences between qualified & nonqualified plans.

Executives often utilize nqdc plans to defer income taxeson their earnings. If there is a wide pay gap between your upper management personnel and your rank and file employees, you may consider offering both a qualified retirement plan, such as a 401 (k) or simple ira, and a nonqualified plan. There is a different set of rules for a qualified plan vs. This type of policy becomes paid up once a certain amount of premium has been paid into it. Contributions to qualified 401 (k) and 403 (b) plans are capped at $19,500 in 2021, the same as 2020. But, both are handled very differently. Differences between qualified & nonqualified plans. In other words, all of your earnings on an non qualified annuity will not trigger an annual 1099 tax form from the annuity company. Benefits received on or after january 1, 1997 will not be taxed, even if they: A nonqualified plan can provide deferred payments at a specified future date, allowing you to save for certain life events, such as a child's college education. Could i benefit from deferring income taxes until a later date? Nqdc plans (sometimes known as deferred compensation programs, or dcps, or elective deferral programs, or edps) allow executives to defer a much larger portion of their compensation and to defer taxes on the money until the deferral is paid. A nonqualified (nq) plan is simply a plan that does not qualify under internal revenue code (code) section 401 (a), which includes standards for who can participate in the plan, how benefits are accrued, vesting schedules, distribution options, etc.